Welcome to the new issue of Grow Your Knowledge Newsletter where you get free, ready to use, actionable, clear information regarding FIDIC Contracts and Construction Claims.

Today at a Glance;

➤ Term of the Week

➤ One Tweet

➤ What are the sources of Financial Information while quantifying the claim?

TERM of the WEEK

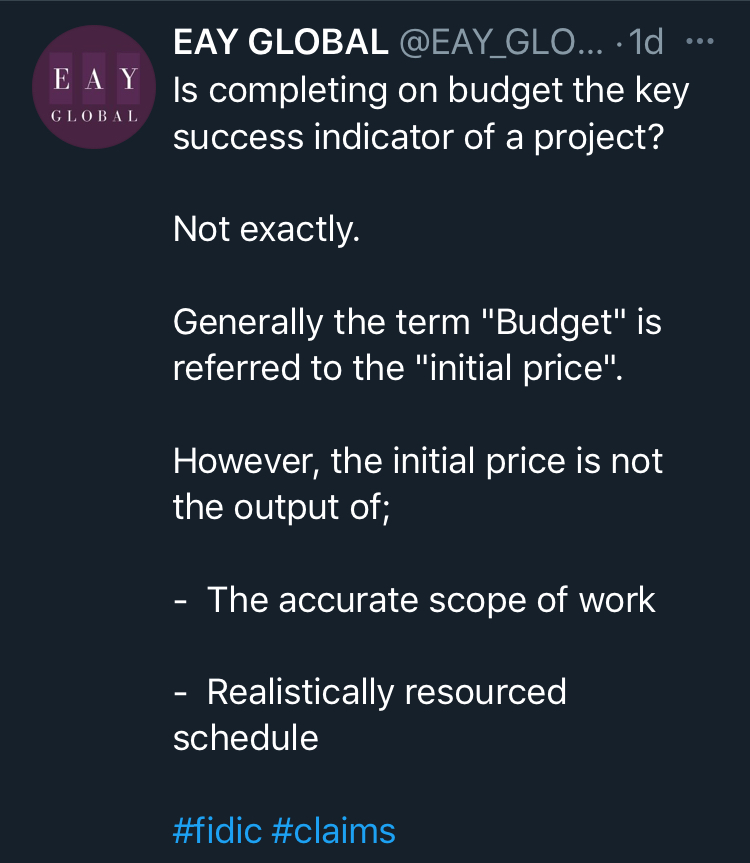

ONE TWEET

The SOURCES of FINANCIAL INFORMATION while QUANTIFYING the CLAIM

Properly quantifying the claim is vital for the effective claim.

Accurate financial information is essential for proper quantifying.

But, what are the sources of such financial information?

You should consider using a variety of resources for that, such as;

➤ The Contract Provisions

➤ Tender Calculations

➤ Cost Records

➤ Accounting Information

➤ External information

SOURCE 1: The Contract Provisions

The starting point must be the terms and conditions of your contract in connection with;

➤ Express provisions of the agreement

➤ Any terms imposed by applicable law

Furthermore, you have to check the definitions of the terms;

➤ Cost

➤ Loss and Expense

and understand if there is any change in the accepted or assumed meaning of these terms.

## Cost ##

The term “cost” is commonly used in contracts and most commonly relates to evaluating some types of claims for additional payment, both for;

➤ The direct consequences of a variation, and,

➤ The indirect effects on the programme of works and productivity

## Loss and Expense ##

“Loss and Expense” is a term that may be interpreted in different ways.

Because of that, it should be defined clearly.

If there is no sufficient definition regarding the meaning, it will be difficult to answer the questions;

➤ Is the profit included?

➤ Is the financing charge included?

SOURCE 2: Tender Calculations

You should examine the tender calculations.

While doing that you should consider all the information regarding the calculations underlying the contract pricing.

SOURCE 3: Cost Records

The main source of cost information on a construction project is the Contractor’s cost documents and accounting records for that project.

You should consider;

➤ Identification of Invoices

➤ Discounts

➤ Bulk Discounts

➤ Timing of Costs

➤ Final Accounts

## Identification of Invoices ##

If any invoice is used as a source of costing you should clearly identify the project which it is related to.

The invoice should also clearly describe the details of the material, goods, plant, equipment or other source supplied.

Additionally it should determine the point of delivery.

## Discounts ##

Most invoices will state the amount of any types of discount relevant.

That kind of discount should be deducted.

Comparison of the invoice amounts with payment records will usually establish this.

## Bulk Discounts ##

When the supplier offers a discount which is refunded as a credit against the Contractor’s account when a specific level of business is achieved;

➤ Checking that kind of bulk discounting becomes a difficult task.

## Timing of Costs ##

Contractor’s cost accounting systems probably record the cost;

➤ by invoice date, or,

➤ by the date that the cost is entered into the system.

However, if the expenditure needs to be examined in particular periods, these can cause problems.

## Final Accounts ##

Another main source of information is the final accounts agreed by the Contractor with its various Subcontractors and Suppliers.

SOURCE 4: Accounting Information

The accounting records usually provide two types of information available: these are;

➤ Financial Accounts

➤ Management Accounts

## Financial Accounts ##

Financial accounts are the ones that are produced and submitted to the regulatory authorities of the country.

They usually comprise two elements;

- The Profit and Loss Account

- The Balance Sheet

Profit and Loss Account shows the income and expenditure in the accounting period with any adjustments or other charges (such as overheads/administration costs and financing charges) and other income required by the accounting practice.

The Balance Sheet shows the available funds, their sources and the place where they are used.

## Management Accounts ##

The management accounts are much more extensive and detailed than the financial accounts.

They record the income and the expenditure in much greater detail.

SOURCE 5: External Informatıon

Some of the examples for external information are;

➤ Pricing books

➤ Records from the Contractor’s other projects

➤ Data from the wider market

Consequently all you have to do is;

➤ Reviewing the contract carefully

➤ Clearly understanding which of those financial information are relevant

➤ Properly quantifying the claim

See you next week.

P.S. As always, we hope you find this issue useful and we welcome any comments or feedback you may have.

![Delay Claims Preparation [Checkpoints]](https://eayglobal.com/wp-content/uploads/2024/05/1-150x150.jpg?crop=1)